Theory vs. Practice

You've got a lump sum of money sitting in cash. Invest it all at once, or dollar cost average in?

In 2019, Mother Cabrini Health Foundation was a brand-new foundation, set into existence with roughly $3.2 billion of capital. The back story of Cabrini is a good one, but that’s for another day.

For the investment team stepping into Cabrini, our mandate was clear. The foundation’s $3.2 billion was predominantly held in Treasury bills, and the portfolio needed to be built out across asset classes and investment strategies. In other words, turn a cash portfolio into an endowment portfolio.

There were many nuanced decisions that we had to make as we built the portfolio in those early days. There was also a seemingly simple one that we knew carried potentially significant consequences: after determining the desired public equity exposure for the portfolio, should the investment be made in a lump sum, or through dollar cost averaging over time?

This week’s question brought me back to Cabrini’s early days.

Hear more of the Cabrini story in my interview with Cabrini CIO Colin Ambrose:

available on YouTube, Apple Podcasts, and Spotify

I have an account sitting in cash, it’s for [a personal reason]. I want to put it in the stock market, but it doesn’t feel like a great time to start. I’m not planning to take money from the account anytime soon, for years, but I’m also not planning to add money to the account again. What would you do?

I’ll do one better, I’ll tell you what we did.

The starting conditions for Cabrini were pretty similar to yours. Sure, Cabrini’s portfolio might have been orders of magnitude larger, but we had a lot of the same considerations. We had an account in Treasuries. Foundations are closed pools of capital, so there would be no additional inflows. Cabrini did have a spending policy almost from day one, meaning some dollars would be drawn from the account each year, but the equities part of the portfolio was intended for growth, not spend. And equity markets looked richly valued in 2019 too.

That said, history told us equity markets tend to go up over time. Plus we philosophically didn’t believe in trying to time the market.

Let’s pause here for a moment and run some numbers. If we look back at past markets, make a few assumptions, and run some scenarios, what would the data tell us? Is there a theoretically correct answer to whether an investor should invest all at once or gradually over time?

I’ll use some super basic assumptions:

An investor starts with $1,000,000 in cash.

The only equity investment will be in the S&P 500 Index.1

Any money not invested in the S&P 500 earns a short-term yield, approximated using the Fed Funds rate.

The money stays invested for 10 years.

Let’s say the investor has two choices for investment approach:

Lump Sum: invest all $1,000,000 into the S&P 500 on day 1.

Dollar Cost Average: invest an equal amount into the S&P 500 every Friday for 52 weeks, averaging in over the course of a year.2

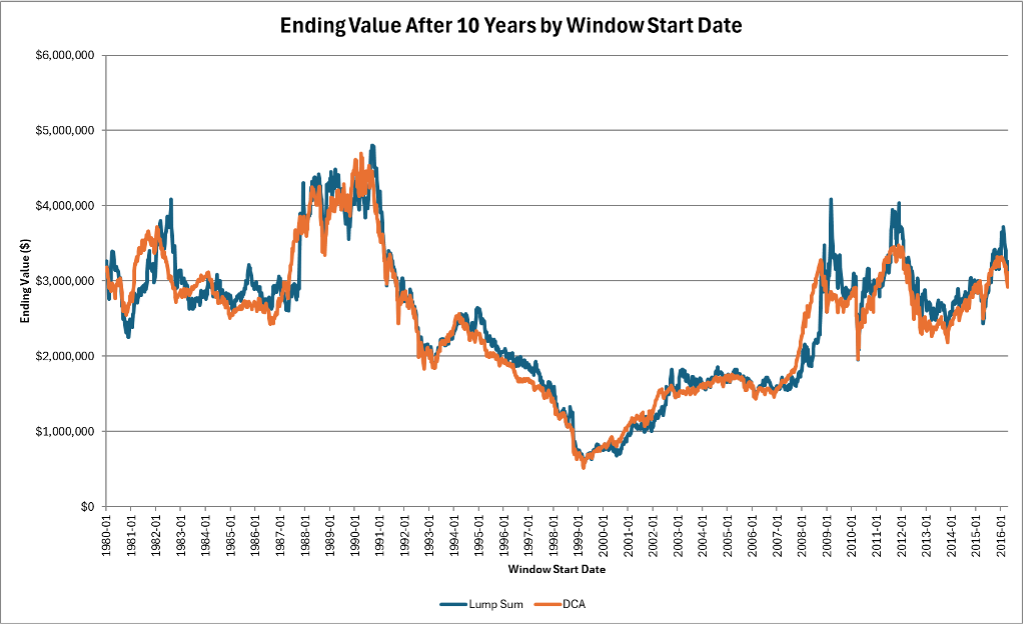

If we start in 1980, and look at every rolling 10-year period (on a weekly basis), which investment approach results in a higher portfolio balance at year 10?3

Quick takeaways from the graph above: in the majority of cases, the lump sum approach won out, but the average difference was smaller than you might think. And dollars invested in the S&P 500 from late 1998 to early 2001 were worth less 10 years later.

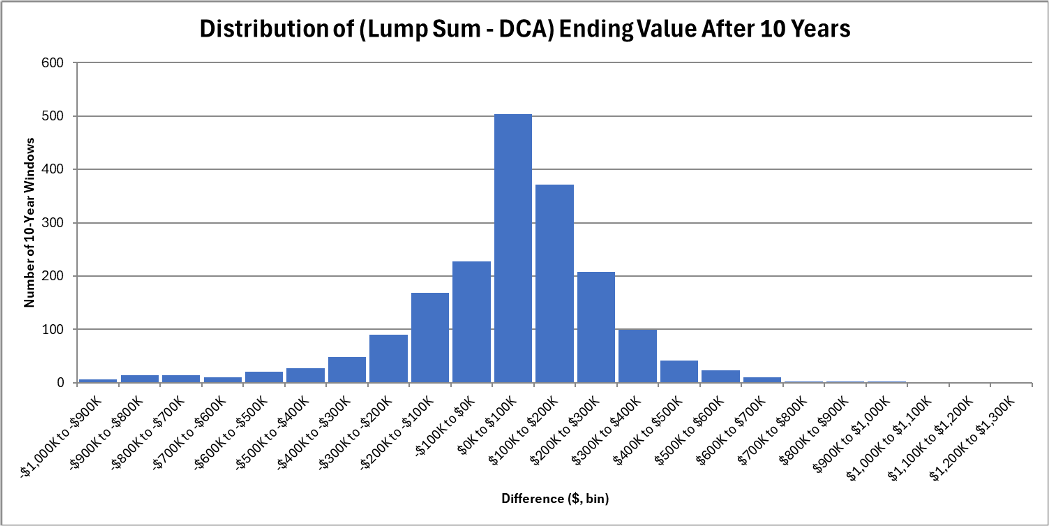

Breaking it down a bit further, the chart below shows the distribution of outcomes, as measured by the difference in ending portfolio values. A positive difference reflects outcomes where the lump sum ending balance exceeded the dollar cost average ending balance.

Once again, we see that in the majority of cases, the lump sum approach won out, most commonly by an amount that was less than $100,000 after 10 years. It is notable that the left tail is a bit fatter, suggesting that when the dollar cost average approach had a better result, it could be by a lot.

In summary, the lump sum approach won ~67% of the time, with a median difference of ~$59,000 dollars. For my own sanity, I ran a fairly simple analysis here with a basic set of assumptions. But I have reasonable confidence that these conclusions are directionally correct and would hold under a range of other assumptions.

From a theoretical, expected value standpoint, the correct answer is almost certainly that an investor should invest in equities with a lump sum approach.

But that is actually not my answer. Or at least, not my complete answer. As investors, we don’t operate in theory, we operate in practice.

In practice, we cannot predict the equity market ahead of us. In practice, investing ahead of a stock market downturn is a real and rational concern.

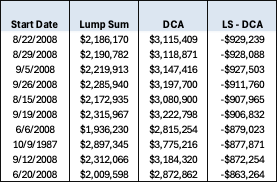

The table below reflects the 10 worst windows for lump sum investing as compared to dollar cost averaging. No surprise, investing everything all at once before the worst of the Global Financial Crisis resulted in meaningfully lower outcomes.

Portfolio Ending Value After 10 Years

Going back to where we started – what did we do at Cabrini?

We chose to dollar cost average into our public equity exposure. We weren’t perfectly formulaic, and we didn’t take a year, but we were consistent over the time period we chose. We had an allocation framework in mind, and we progressed toward it in a disciplined way that removed the element of market timing.

In theory (and in hindsight), investing all at once into our full equity allocations would have produced the highest expected value, but the risk of prolonged capital impairment was not acceptable to the foundation. We made the right decision for the foundation at the time, and I have no doubt that we would do the same again under the same fact pattern. As a good friend and mentor would frequently remind me – it’s not just the probability, it’s the consequence.

As for your portfolio, only you can answer the question of how much you care about either the probability or the consequence of potentially investing ahead of a downturn. There’s no way to know ex-ante what kind of market you’ll be investing into. But no matter what you decide, whether you choose to invest all at once or over time, I do think that making the choice to get invested is almost certainly better than sitting on the sidelines.

Thanks for the great question! Please reach out with more: askacio@ivyinvest.co.

See you in two weeks,

Wendy

If you enjoyed this post, you might also enjoy the Ivy Invest app!

Click below to create an account and learn more about our endowment-style fund:

Let’s say dividends are not reinvested for my ease of use. Pre-1990 data is easier to work with assuming dividends are not reinvested.

About $19,230 each week, with any residual cash from interest earned throughout the year to be invested at week 52.

Why start at 1980? No particularly scientific reason. I wanted to capture the savings and loan crisis, the dotcom boom and bust, and the GFC.